Manufacturers, make your brand portfolio work again in China

6 July 2020 — Consolidating Reddal’s learnings in China from the past few years, this article shares some observations on the dynamics of industrial goods market segmentation. It offers a continuous and iterative approach for industrial players to respond to these changing market aspects by revising their brand portfolio strategy.

Problem

Industrial goods manufacturers, who have been slow to market changes, find their brand portfolio becoming weaker or ill-fitting in the evolving market in China. At the same time, local players are increasing their competitiveness.

Why it happens?

Mid-market segment is expanding at the cost of high-end and low-end markets, whereas players in the high-end market edge downwards with more competitive localized product lines while low-end leaders rapidly rise to higher segments.

Solution

Industrial players can employ an iterative approach to revise their brand portfolio strategy by understanding customer needs, assessing portfolio against competition, and introducing adjustments systematically.

Download this post (PDF)

New challenges call for a revised brand portfolio strategy

During the past two decades, the business reality in China has changed so dramatically–especially in terms of domestic market maturity, and intensifying competition from domestic players–that for many foreign companies their pre-defined brand portfolio strategy, or lack thereof, desperately requires an update or even complete revamp.

In some of the worst cases, a foreign company’s brand portfolio strategy is simply a duplication of their global lines. It was a reasonable approach back in the days. However, as the market in China today sees continuous expansion or restructuring, this approach leaves out some emerging segments such as niche or ultra-high-end markets.

Many foreign companies accelerated their pace in entering China at the turning of the 21st century (when China was admitted into the WTO framework), with strategic targets focused primarily on setting up a cost-effective supply chain. While these strategies were solid back then, it is becoming increasingly evident that they struggle to cope with rising challenges and to capture emerging opportunities. One typical limitation we observed is not being able to address the growing domestic mid-tier market and new application/segments. This trend of an expanding mid-tier market (often at the cost of high and low segments) requires dedicated offerings at a fast pace, to which global players often fail or are slow to respond. Losing the competitive edge against local competitors in their own segments, even in previous strongholds, is another limitation. In addition to lower prices and more dedication in service/support (especially for key customers), local competitors often enter a new segment by winning an industry leader (global companies most of the time) at all costs, or even forming a JV to share benefit with the influential customer. As a result, foreign players’ ties with their global accounts are weakened, and in some cases, the impact is already seen beyond China–construction machinery and port crane industries are clear examples. Last but not the least, limitation may come from the lack of flexibility due to a global brand strategy. Adjustment in positioning and business model can be made only after a lengthy process and is often rejected by HQ due to the potential damage on the global brand’s profitability in other markets.

Playing in the B2B market, industrial goods manufacturers often target specific markets. As B2C brands seek to widen their mass appeal, industrial goods manufacturers seek to position themselves as the best choice within a narrow field. When this narrow field changes, industrial goods manufacturers find themselves with a weak and ill-fitting brand portfolio. To be able to make strategic decisions on their own brands, companies need a systematic portfolio assessment approach that reflects customer needs and current competing brands. A three-step approach would serve companies well by first clarifying both customer needs and positions of similar brands for serving these needs, then defining portfolio coverage targets and adjustments required to achieve brand targets, and finally implementing adjustments with a carefully defined plan.

Re-understand markets and customers along the evolution occurring

The starting point is to (re-)understand customer needs in what most likely is a rapidly evolving market. One approach is to collect customer needs comprehensively, to estimate the size of customer needs, and to illustrate the intersection between the needs and current market segments. By doing so, companies go through a reality check to calibrate their view on the market segments and key customer needs driving the segmentation.

Companies think about reviewing customer needs occasionally, but most often they skip revisiting customer needs and defining brands with presets, for example, by price level (such as an economy brand) or segment (for instance, a brand for HVAC customers). Although forming and scrutinizing customer needs are demanding, it often provides a refreshing view of the market, thereby helping companies identify emerging opportunities and issues within their portfolio.

For example, when a global industrial equipment manufacturer scrutinized the customer needs within the HVAC industry, it discovered that the demand for advanced connectivity features is very low–the majority of customer needs are met with an existing “economy brand”. Such findings reveal that “having two brands (premium and economy) per industry” approach can be false and less effective.

Evaluate portfolio coverage and brand position against competition

Illustrating customer demands and segments is nothing more than a descriptive exercise; it represents market opportunities but lacks context for companies. To derive implications on the brand portfolio strategy, companies must overlay competitive landscape, namely brands alike, over customer demands and segments illustration.

Together, these exercises form a comprehensive view of positions and high-level trends of brands alike in various segments of the target market, thereby revealing the portfolio’s current coverage in the market. There are three common portfolio coverages in a market: 1) portfolio covers both “high” and “low” segments (for instance, strong players with multiple brands covering all segments), 2) portfolio covers only the “high” segment (say, niche player targeting a specific range of high segment), 3) portfolio covers only the “low” segment (for example, small player targeting low segment). The definition of “high” and “low” segment varies depending on criteria.

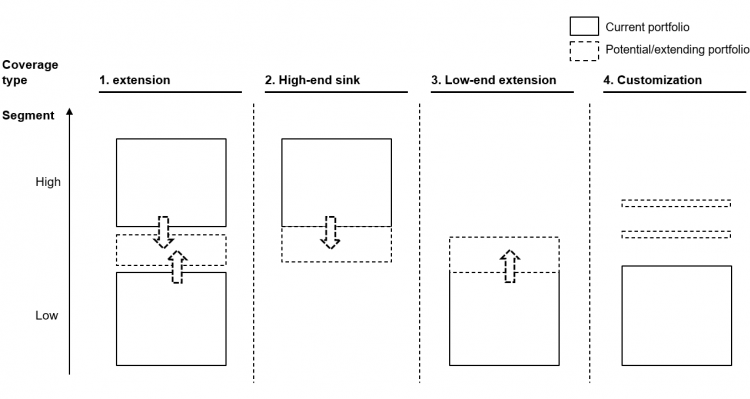

In emerging markets such as China, companies often find the market expanding rapidly, driven by growing demands and increasing standard of living that create a growing mid-segment market. This trend creates a new space between the previously defined “high” and “low” segments. To cover this space, companies have four common options (Figure 1): 1) extend the coverage of “high” and “low” segments to fill the gap, 2) sink brands used to target “high” to “mid” segment, 3) extend brands used to target “low” segment to cover higher segments, 4) create a customized offering that targets the higher segment without changing their brand portfolio.

Figure 1. Options to extend portfolio coverage.

Given the options above, typically there are two types of actions available for companies. Firstly, companies can restructure their existing brand(s) through expansion, repositioning, repurposing, or merging to capture emerging space or recover lost relevance in target segments. Alternatively, they can also cover the gap identified in target segments by launching a new brand or acquiring a value-creating brand.

A company chooses their desired option and actions to capture the newly emerged “mid” segment based on the company’s ambition, position, and performance of its current brand portfolio in the competitive landscape, as well as available resources. However, through observations from practice, brand portfolio adjustment may encounter many challenges. Restructuring can be messy as it requires rethinking the value proposition and reshaping customer perceptions. Introducing a new brand is often riskier and more expensive. Acquisition of an existing brand that fits the purpose falls between them. Thus/therefore, a carefully planned transformation is required.

Define a transformation plan to lead the way forward

Implementing an updated brand portfolio strategy requires diligent effort.

Buy-in and alignment: The strategy must have an endorsement from all brands within the portfolio on both global and regional levels. Incentives that are linked to the portfolio’s overall performance help ensure that all brand owners work for the best of the portfolio. Without a clearly aligned focus, the effort would be diluted by different agendas.

Close follow-up: Measuring whether planned adjustments meet their targets is essential. Standard tracking metrics can reveal customer awareness but can be too generic for tracking brand-specific performance. Tailored metrics are needed as a supplement to complete the view.

Avoid pitfalls: Re-calibrating brand portfolio strategy for one of the largest markets takes systematic efforts and high mandate from top leadership. Challenges from multiple areas might arise if the plan is not thoroughly laid out beforehand, it will not succeed as a single-handed effort. Some of the most critical challenges we observed are:

- Lack of support/misalignment from global-regional strategies

- Complexity in product portfolio management exceeds existing capabilities

- Sales team reluctant to change, with limited interest and capabilities to sell extended/adjusted portfolio

- Channel partners resist the expansion of network - effective fencing measures are needed to prevent cannibalism

- Losing of some existing partners might be necessary to develop new partners with desired capabilities

Switching to a continuous iterative approach

In emerging markets like China, everchanging customer needs create, shift, and even eliminate segments in the market. It is uneasy for companies to feel every pulse of the market. However, for companies that are successful in these markets, iterating portfolio strategy is not a one-time effort. It is embedded in daily operations.

Tags

China, Brand, Brand portfolio, Strategy, Transformation, Industrial manufacturers in China, Market segmentation, Portfolio management, Brand portfolio strategy