China ambitions in cruise sets their agenda for the full value chain

6 September 2021 — China has been actively moving towards the upstream of the value chain with ambitious plans, leaving the industry pondering what will happen next. In this article we try to shed some light on the implications.

Download this post (PDF)

China is not something new for international cruise operators. Carnival, Royal Caribbean and others have spent the past decade penetrating China’s market. Those efforts paid off, with passenger volumes growing rapidly until the coronavirus pandemic swept across the world and brought the industry to a halt.

One cannot fully understand China’s ambition in the cruising industry without a view on China’s activities along the value chain. Here, we collect pieces of the puzzle from the Chinese government and different players along the value chain to discuss implications for players in this industry and its value chain outside of China.

Large cruise ships, a new crown jewel dreamed by the Chinese government

China has impressed the world with the construction of the world’s longest high-speed railway network and its home-made large jetliner. Now the government eyes large cruise ships, the next stage for its high-end manufacturing ambitions.

In June 2008, the National Development and Reform Commission, the country’s top macroeconomic management agency, issued the Guidance of the Promotion for China Cruise Industry Development. In that guidance, it visions the build-up of domestic large cruise ship design and construction capabilities through technology transfer, cooperation and innovation. This was not only about design and construction of cruise ships, however.

In 2013 and 2014, the State Council issued two documents promoting the tourism industry development including the cruise industry.

In 2014, the Ministry of Transportation published the “Guidance of Promotion for China Cruise Transportation Development”. The guidance highlights the importance of developing cruise lines as well as cruise ship design, construction and maintenance. The guidance also relaxed the age limit for imported second hand cruise ships to 10 years.

In 2015, China introduced its Made in China 2025 strategy[1], in which the construction of cruise ships is given a concrete target for the first time on the central government level. In that strategy, key focus areas include “breakthrough in the design and construction technology of cruise ships” and “improvement of the international competitiveness of high-tech ships” within 10 years. The strategy also highlights that China should master the core technologies of providing supporting equipment to shipbuilding. The strategy is a clear indicator that China aims to move upstream along the value chain. To support implementation of such a strategy, six ministries and commissions jointly issued the Opinions on Promoting Tourism Equipment Manufacturing. This document listed accelerating cruise ship design and construction as the first of five key tasks, making it the top priority for industrial development planning. It also pledged to use various funding sources to support cruise ship design and construction related innovation. It also aimed to provide financial and tax incentives for localizing the supply chain of key spare parts.

While Made in China 2025 focused upstream of the value chain, downstream has not been forgotten. In 2016, Chinese central government released an announcement about the 13th Five-year Plan (2016-2020) for Tourism Development[2]. The announcement emphasizes downstream development, focusing on infrastructure development, cruise port reception and management, as well as cruise tourism. The same policy was highlighted again in the 14th Five-year Plan (2021-2025)[3]. It is clear that China aims to establish a complete cruise ship value chain, which creates job opportunities, establishes a new supply chain, and promotes technology innovation. A key driver is also to improve local tourism opportunities, benefitting Chinese economy both by keeping Chinese spending their money at home, and attracting foreign currency. The National Coastal Cruise Port Layout Plan[4] released in 2015 by the Ministry of Transportation sets the ambition to build 12 departure ports and 2-3 cruise homeports by 2030.

It is important to understand the above commitments in the context of the overall process of national strategy implementation. In China, while the central government introduces the strategies and policies to set the direction, it is up to local governments to detail and specify for implementation. Major Chinese port cities have introduced their action plans. Cities such as Shanghai[5], Xiamen[6], Tianjin[7] and Sanya[6] focus on downstream development, highlighting the cruise port development and tourism products for cruise ship passengers. Cruise operation is a very profitable business and has a great economic multiplier effect to all harbours and locations that are on the itinerary. It is not a surprise to see the strong support from local governments to attract and develop downstream business.

The state calls and the state-owned shipyards answer to the massive engineering challenge

Those who are not closely following the development patterns and political system structure of China may have difficulty understanding the implications of these policies. Sure, China has dumped the core of its communist economic system a long time ago, replacing rigid central planning with commercially minded state enterprises that coexist with a vigorous private sector. One must remember that despite all the achievements from economic liberalization, the Chinese Communist Party has been careful to keep control and hold the helm while steering the nation forward. The central government sets the high-level vision, which then is translated into concrete actions by Ministries and lower-level governments. Once all levels are aligned, enormous resources are pooled together for implementation. State enterprises play a key role in such implementation and P&L is never a top concern. This process tends to take time, and often initial movement is slow, but once all resources are aligned development accelerates rapidly. Although all countries support their shipbuilding business, China is approaching this more systematically and strategically than others with strong alignments with key stakeholders and clear targets.

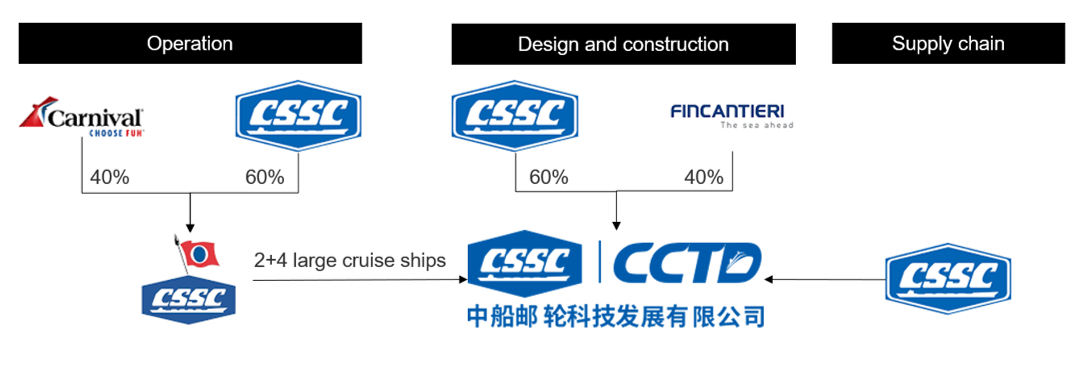

China’s plan to promote the development of large cruise ships follows the same pattern. Driven by the strong vision from top-level government, massive state enterprises are mobilized. China State Shipbuilding Corporation (CSSC) started a cruise ship construction project in 2012, backed by China Investment Corporation and other state-owned banks such as the Export/Import Bank of China, seeking for partners worldwide. Eventually CSSC signed a memorandum with Carnival and Fincantieri in 2016 and updated it in 2017. The memorandum defines a mechanism to share potential risks associated with the construction and to provide maximum benefits to partners in exchange of technologies and expertise. A joint venture, the CSSC Carnival Cruise Shipping, between CSSC (60%) and Carnival (40%) purchased two cruise ships (and four options) from another joint venture, the CSSC Cruise Technology Development (CCTD), between CSSC (60%) and Fincantieri (40%) which is responsible for design and construction[8]. The ships are built in CSSC’s flagship shipyard, Waigaoqiao Shipbuilding, in Shanghai. See figure 1.

It is believed that Carnival and Fincantieri have secured a position in the promising Chinese market through this joint venture structure. Through the CSSC Carnival Cruise Shipping, Carnival could gain access to top decision makers in the government and build a fleet of eight cruise ships (including two second hand cruise ships purchased from Costa) by 2027, largely funded by Chinese partners. With the joint venture, Carnival could also get an exemption from Chinese laws that ban foreign vessels from doing business between Chinese ports. This will be a significant advantage for Carnival. In 2018, nearly 2.4 million people in China went on a cruise and the majority of them were on international fleets. The recovering tourism industry and the limitations of the corona pandemic provided strong incentives for domestic routes. China resumed cruises in December 2020 with routes starting from and finishing in the Chinese resort island of Hainan without any stops in between. So far, only Astro Ocean International Cruise[9], a joint venture between two state-owned companies, has been awarded a permit to operate. Other cruise operators are following. Viking Cruises has teamed up with China Merchants Group to form the China Merchants Viking Cruises. The joint venture received their first cruise ship, Viking Sun, in April 2021 aiming to operate itineraries from Chinese homeports. After receiving Costa Atlantica from Carnival in 2020, CSSC Carnival Shipping launched the route from Shanghai to Japan, however it was shut down by global travel restrictions. With another ship, Costa Mediterranea, transferred in April 2021, CSSC Carnival Shipping is now eyeing a permit for domestic cruise route operation.

Fincantieri, CSSC’s partner in design and construction, has deep expertise in cruise shipbuilding. The shipyard has the biggest share of cruise ship order books in the market. Its decision to join forces with CSSC for Chinese homegrown cruise ships has surprised the industry. The decision is considered to be a case of prisoner’s dilemma by many, as it could intensify the competition in the global cruise shipbuilding market by opening the gate for Chinese shipyards. However, Fincantieri clearly has a different opinion. In 2019 there were over 155 million outbound tourists from China[10] of which only about an estimated 2 million were with cruise ships. However, cruising volume has been growing at a CAGR of 38% between 2013 and 2018. International cruise operators are optimistic about market outlook, thanks to China’s large and increasingly wealthy population. The effects of the pandemic are viewed by most as temporary. By inking the joint venture agreement and exporting over 150 000 pages of design drawings and construction management documents (weighing over 2 tons!) to CSSC[11], Fincantieri successfully penetrates and secures its share of the enormous demand potential for the years to come.

Doomsday or opportunity – implications for players outside of China

Many fear that China’s entering the cruise ship building sector may disrupt the market with its relatively cheap and abundant labor force and raw materials. It could be a doomsday scenario for many established shipyards and suppliers. However, the facts provide a different perspective. Shipbuilding is not in a zero-sum game - a significant growth in demand is expected in the long term, both driven by China and other markets. Established European shipyards most likely will not feel much competition from China in cruise ships during next two decades, given substantial growth in demand from China, limited cruise ship construction capacity and cost challenges due to an immature supply chain.

Despite the pandemic, people are optimistic and pent-up demand is out there. China, the fastest growing cruise market, is expected to become the world’s largest cruise market by 2030. In 2019, there were 22 cruise ships serving the Chinese market, serving over 2.4 million passengers annually. Passenger volume is expected to reach between 10 to 20 million passengers per year.

To serve such a volume, there is a demand to at least triple the amount of cruise ships in the market year-round. Such demand is expected to exceed what Chinese shipyards can supply. In an interview with the state media, Zhou Qi, vice-president of Shanghai Waigaoqiao Shipbuilding, said there is substantial room for shipbuilders to participate with current annual global delivery capacity of about seven cruise ships against the demand for some fifteen. Today, only two of CSSC’s shipyards in China have potential for constructing large cruise ships. The first ship is being constructed in Shanghai Waigaoqiao Shipbuilding. The shipyard was founded in 1999, covering five million square meters with four thousand kilometers of coastline. It has four outfitting piers, three docks and eight gantry cranes with over 600 ton capacity. Wholly owned by CSSC, the shipyard ranks as number one in China in terms of volume. To meet the requirements of cruise ship construction, the shipyard has gone through massive reconstruction costing about 265MUSD. The other company that has potential for large cruise ship construction is Guangzhou Shipyard International (GSI). The company is a publicly listed with CSSC being the biggest shareholder. The company has three shipyards with two 300k ton docks, four outfitting piers, and four 600 ton gantry cranes. GSI has no intention to enter large cruise ship construction but focuses on roll-on/roll-off passenger vessels while supporting the Shanghai shipyard. In addition, there are three shipyards with experience in cruise ship refurbishment. However, they are not capable of facing this massive challenge. China Merchant Group is another potential player for the cruise ship sector. The group is involved in developing the full cruise value chain with shipyard, cruise operation and homeports development. China Merchants Cruise Shipbuilding Haimen base has a production capacity of 220 000DWT. The shipyard delivered the first ever Chinese-built, Polar-class expedition cruise ship, part of SunStone’s order for a series of Infinity-class vessels in 2019[12]. With an order book of three expedition vessels (three delivered) and potential four (and four options) mid-sized cruise ships for China Merchants Viking Cruises, the shipyard is preparing itself for tackling the large cruise ship building challenge in the next 5-10 years.

In 2016, Japan’s Mitsubishi Heavy Industries abandoned its ambition to build large cruise ships after a delay of more than one year and costs overrun by almost 2BUSD. One major cause of this failure was an unsuccessful local supply chain. Building a large cruise ship involves about 25 million components and parts, more than 500 suppliers and well over 10 million manhours. In terms of the number of components and parts, large cruise ships are more complicated than China’s C919 passenger aircraft, which contains about 3-4 million components. To avoid repeating past mistakes of underestimating technology build-up efforts needed, CCTD has pursued close collaboration with Fincantieri and Lloyd's Register of Shipping. However, due to an immature domestic supply chain, the project still relies heavily on established suppliers outside of China, causing challenges especially during the pandemic. Suppliers are selected from the preferred supplier list drafted by the owner, shipbuilder, designer and engineering company. Most supplier candidates come from Fincantieri’s supply chain. A joint team from procurement, technical, finance and legal at shipyard evaluate candidates and propose selection. The final decision is made by the yard’s top management.

During construction of the first two cruise ships, CSSC wants to establish its own supply chain. Developing and promoting local supply chain is a pressing issue for CSSC to reduce cost to a competitive level. Interior package accounts for more than 40% of ship’s cost. Due to import duty and logistics, using European companies with European materials for outfitting is significantly more expensive for Chinese shipyards than for European shipyards. CSSC is leveraging the joint venture with Carnival to promote localized materials and turnkey contractors.

"Our collaborations with our foreign partners are targeting new demand coming from China. Opening-up and collaborating does not conflict with innovation on one's own. We will make innovations in our products, but that does not mean we have to do all the work by ourselves. As a matter of fact, it would be better if we get the work done by working together" says Wang Yanguo, vice-president of CSSC Cruise Technology Development.

For established European suppliers, now is the time to evaluate and decide whether to enter the Chinese market with local presence. Entering a market like China takes time and resources. However, established European players have advantages with their expertise and track record to establish relationships with Chinese shipyards. While the emerging market offers enormous opportunities, there are risks as well. Technology transfer and IPR infringement remain key challenges for foreign players when entering the Chinese market.

The Chinese are stepping up – time for the industry to do the same

The Chinese government is seriously committed to master large cruise ship construction. This is happening regardless of the initial cost, since there are larger national interests at play – mostly related to Chinese domestic economy. However, it will take time before Chinese yards can compete with established ones in Europe, given project complexity and immaturity of the domestic value chain. Also, we believe Chinese shipyards will focus on emerging domestic demand in short- to mid-term. In the long term, we see increased global demand with room for strong players. In an industry like shipbuilding the game is never fully fair due to national interests, but there is room for those who decide to continue to step up their game. Further, for foreign cruise shipbuilding (component and turnkey) suppliers, the emergence and growth imperatives of the Chinese cruise ship value chain provides a potentially lucrative opportunity. However, the train is moving. Thus, now is the time to make the analysis and strategic decisions.

References

[1] The State Council of The People’s Republic of China (2015), retrieved at http://www.gov.cn/zhengce/content/2015-05/19/content_9784.htm on 23 August, 2021

[2] The State Council of The People’s Republic of China (2016), retrieved at http://www.gov.cn/zhengce/content/2016-12/26/content_5152993.htm on 23 August, 2021

[3] The State Council of The People’s Republic of China (2021), retrieved at http://www.gov.cn/xinwen/2021-03/13/content_5592681.htm on 23 August, 2021

[4] The State Council of The People’s Republic of China (2015), retrieved at http://www.gov.cn/xinwen/2015-04/28/content_2854090.htm on 23 August, 2021

[5] Shanghai Government (2018), retrieved at https://www.shanghai.gov.cn/nw44084/20200824/0001-44084_57380.html on 23 August, 2021

[6] People’s Daily (2019), retrieved at http://travel.people.com.cn/n1/2019/1031/c41570-31429890.html on 23 August, 2021

[7] China securities news (2020), retrieved at https://news.cnstock.com/news,bwkx-202009-4590642.htm on 23 August, 2021

[8] CSSC Shanghai Waigaoqiao Shipbuilding (2018) press release, retrieved at http://cn.chinasws.com/component_news/news_detail.php?id=1474 on 23 August, 2021

[9] Astro Ocean Cruise (2020), press release, retrieved at https://www.aocruise.com/detail/25 on 23 August, 2021

[10] China statistical yearbook (2019)

[11] Shanghai Baoshan District Government (2019), retrieved at http://www.shbsq.gov.cn/shbs/rdtj/20191025/209109.html on 23 August, 2021

[12] China Merchants Group (2019), retrieved at https://www.cmhk.com/main/a/2019/c12/a37671_38332.shtml on 23 August, 2021

This topic was also covered by Finnish business newspaper Kauppalehti in an article "Pettikö Fincantieri Euroopan?" on October 4, 2021.

Tags

China, Cruise ship, Shipyard, Made in China