When traditional manufacturers encounter digital disruptors: collaborate and compete on industrial digital solutions

23 June 2020 — The market landscape of traditional manufacturing companies has been facing large scale digital disruptions. This article discusses the patterns of disruption and suggests a potential response strategy.

Problem

Traditional manufacturers find it difficult to create sensible, scalable and competitive digital solutions that customers are willing to pay for.

Why it happens?

Digital disruptors with strong competence in data management and analysis are penetrating the market for industrial digital solutions, which substitutes the demand for offerings of the traditional manufacturers.

Solution

Traditional manufacturers should consider a strategy of leveraging the competence of digital disruptors to fill own competence gaps, while defending the markets that require strong substance knowledge and control over installed base.

Download this post (PDF)

Digital disruptions in manufacturing

Digital technologies are not completely new to the manufacturing sector. In practical work we often receive comments from industrial representatives such as “IoT is nothing new”, “we started using smart sensors and an automation system decades ago”, and “our products today can generate and collect data”. These comments indicate that manufacturers not only are familiar with digitalization but also may even have initiated the application of specific digital elements in their business.

However, in the past decade, digital technologies have triggered a massive amount of new market opportunities and expanded the competition beyond the traditional device business[1]. Digital technologies enable the generation and collection of longitudinal data from devices, which provides raw material to be further investigated and exploited[2]. As an example, data analytics can be applied to improve the efficiency, accuracy, and performance of devices while minimizing human intervention. Such solutions built on top of data are expected to bring remarkable value creation opportunities to manufacturing companies. However, unlike the traditional device business, the competitive landscape in this field has become turbulent due to disruptions from new entrants. This disruption is associated with not only fast-evolving digital technologies, but also the business model, as well as business logic changes in economic and social contexts.

“Cross the sea without the emperor's knowledge.” - Thirty-Six Stratagems

There might be the inertia of thinking that traditional manufacturers are the natural data solution providers for their devices. However, the reality seems more complicated. On the one hand, many traditional manufacturers are struggling to create sensible and scalable digital solutions that customers are willing to pay for. On the other hand, platform providers and data analytics companies have entered the market with strong competences in data analytics and management. Such patterns indicate that we need to re-evaluate the competitive landscape of solutions based on industrial data and the role of traditional manufacturers in the ecosystem.

Stereotypical penetration patterns of digital disruptors to traditional manufacturing market

Based on our observations, we see three types of digital disruptors entering the digital solution market for traditional manufacturing sectors: platform providers (PPs), managed service providers (MSPs), and data analytics companies (DACs). PPs are tech giants such as Amazon, Microsoft, and Google, who provide general purpose technology and platforms on which digitalization is built. PPs have enjoyed strong market growth during the last five years, as many companies are gradually migrating to cloud solutions. For example, Microsoft’s cloud segment revenue grew on average 13% during 2015 - 2019 from 23.7BUSD to 38.9BUSD, whereas AWS performed at an astonishing 45% average revenue growth, growing from 7.9BUSD to 35BUSD in the same period[3] [4]. These integrated platforms provide the fundamental building blocks for companies to manage data from various sources. In addition, available technology toolsets such as API management, cognitive algorithms, and cloud computing within the platform significantly shorten the development and deployment of digital applications.

MSPs, such as Accenture and CGI, have traditionally been important IT service partners for corporates and are uniquely positioned to support them in their digital journey. The market for IT services has grown from 866BUSD in 2015 to 1.03TUSD in 2019[5]. MSPs can provide cost-efficient services, given their offshore model as well as extensive internal knowledge and toolkits for developing digital solutions. MSPs provide services based on the specific customer demands, which makes the order vary significantly in scale. Nevertheless, they are often selected as partners for corporate level digital transformation projects because they are capable to serve the various capability demands throughout the transformation process.

Lastly, data analytics companies have entered the realm of industrial digital solutions market leveraging their analytics capabilities. They are the driver behind continuous returns by experimenting with their data to develop value. Operating under this “fail fast, learn faster” philosophy, DACs adopt an agile and innovative approach in piloting digital initiatives. For example, Delphix optimized data flow for Facebook that culminated in Facebook CRM and Audience Insights, resulting in 40BUSD in revenue [6]. Similarly, this is how DACs penetrate traditional manufacturing. We have observed that DACs are already deeply involved in industrial digital solutions for heavy industries and automotive manufacturing. Given that in the past decade a large number of traditional manufacturers have not treated data as a valuable asset but rather as a “liability” which just needs to be stored somewhere, DACs have enjoyed the opportunities to aggressively to expand their presence in industrial digital solutions.

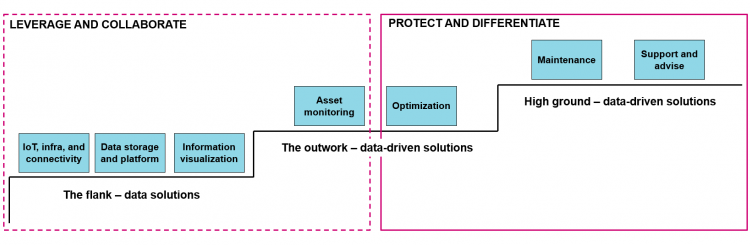

Depending on the solution characteristics and associated capability requirements, we consider that the industrial digital solutions can be divided into two categories: data-solutions and data-driven solutions, see Figure 1. Data solutions are associated with collecting data and forming the basis for data-driven solutions. Offerings such as IoT, infrastructure and connectivity, as well as data storage and platform ensure that data is collected from industrial assets and is stored for further use, while information visualization translates the data into the forms which are made understandable by human users. Data-driven solutions are purposeful applications for value creation that use collected data. They can be further divided depending how this value creation is created, as the following: asset monitoring, optimization, maintenance, and support and advise. Remote monitoring solutions track physical assets via sensors and other means. Optimization solutions create value by increasing the efficiency of the production process leveraging data. Maintenance solutions predict maintenance needs or asset failure in advance so measures can be taken. Support and advise solutions provide support customers via digital means, for example AR/VR. It is important to note that opportunities in digital manufacturing are sequential; in other words, without data solutions it would be impossible to provide data-driven solutions.

Based on our observations, the stereotypical penetration patterns of digital disruptors reflect the sequential relationship between data solutions and data-driven solutions, see Figure 1. Data solutions are easily penetrable by disruptors, whereas data-driven solutions are not as easy to penetrate depending on the substance knowledge required for value creation. Firstly, we consider the data solutions are “the flank” for penetration. This is mainly because digital disruptors tend to have more suitable resources and competence in this area, which is not necessarily the case for many traditional manufacturers. Second, some data-driven solutions are natural extensions of data solutions. Examples are asset monitoring and optimization, where processed data can be easily applied to the manufacturing process. These types of data-driven solutions are “the outwork” which has a moderate barrier of entry. Finally, there are data-driven solutions that require industry specific substance knowledge and an install-base. Maintenance and support and advise fall into this category. As a prerequisite to offer digital solutions as such, the suppliers need to have in-depth substance knowledge in industrial applications or have direct access or control over physical assets. Therefore, these areas are the “high ground” which would be difficult for digital disruptors to penetrate.

How traditional manufacturers react to disruption

Disruptors in digital solutions should not be perceived in a completely negative manner, although the disruptors to a certain extend did diminish industry boundaries and have gotten involved in the traditional playground of the manufacturers. Instead, digital disruptors have brought pervasive digital technologies, cross-industry experiences and digital competences that help the industry make advances in digital transformation. This makes them the competitors of traditional manufacturers, while providing complementary digital competences that many traditional manufacturers do not have. Considering this situation, we propose a response strategy on how traditional manufacturers could react to the digital disruptors, see Figure 2.

Given that the disruptors’ strengths are on data solutions, they are able to provide mature, cost-efficient cloud platforms, IoT network, and application development tools. Then, manufacturers should consider directly adopting these offerings or collaborating with disruptors instead of starting from scratch. The world of digital solutions today is quite different from what it used to be 5-10 years ago. Barring some critical applications (such as military applications), it may not make economic sense for manufacturers to reinvent the wheel.

On the other hand, manufacturers need to defend their market presence in the “high ground” where they have competitive advantages on the industry know-how and business network. This is also the area—if done properly and successfully—that will bring huge value to the manufacturers’ customers, and in turn will provide good opportunities for manufacturers to get their share on the value.

However, collaboration is easy to recommend but difficult to do, as traditional manufacturers may have strong concerns about their intellectual properties, and the digital disruptors may be able to “monopolize” the business once they have access to massive amount of business-sensitive data. Therefore, negotiation on intellectual property ownership and customer access should be clarified as clearly as possible.

The ecosystem is forming up now in many industries. If you are a traditional manufacturer and are still hesitating about the situation, we recommend checking two example industries which represent two directions, and see where you see the industry is going to:

- Personal computer – in which the OEM opportunity is capped to only providing hardware, and the software layer is provided by platform providers and app developers)

- Marine industry – in which OEMs are highly relevant and still considered as the main players in Vessel digital solutions

A balance between competition and collaboration

In conclusion, traditional manufacturers should acknowledge the increased presence of digital disruptors in the manufacturing sector and be wise to collaborate with them. However, traditional manufacturers should protect their market presence by creating customized digital solutions based on their substance know-how to maximize the product life-cycle value for their customers. Given that it may be no longer viable for traditional manufacturers to provide every single solution for their products, specialized players should be leveraged by traditional manufacturers to build the basis that enables their digital solutions. Then, traditional manufacturers would be able to reap the fruits of digitalization without reinventing the wheel.

References

[1] Sebastian, I.M., M. Mocker, J.W. Ross, K.G. Moloney, C. Beath, and N.O. Fonstad. “How Big Old Companies Navigate Digital Transformation”, MIS Quartely Executive 16(3), 2017, pp. 197–213.

[2] Xu, L. Da, W. He, and S. Li. “Internet of things in industries: A survey”, IEEE Transactions on Industrial Informatics 10(4), 2014, pp. 2233–2243.

[3] Holst, A. “Microsoft’s intelligent cloud revenue worldwide 2015-2020”, Statista, 2020. Retrieved from http://www.statista.com.

[4] Clement, J. “Amazon Web Services: year-on-year growth 2014-2020”, Statista, 2020. Retrieved from http://www.statista.com.

[5] Holst, A. “IT services global spending forecast 2008-2020”, Statista, 2020. Retrieved from http://www.statista.com.

[6] Bean, R. “Every company is a data company”, Forbes, 2018. Retrieved from http://www.forbes.com.

Tags

Digital transformation, Digitalization, Digital disruption, IoT, Digital solutions, Service development, Manufacturers, OEM, Digital disruptors, Market dynamics, Market disruption