Vietnam’s semiconductor: How domestic leaders can deepen value amid escalating trade pressures

31 October 2025 — Vietnam’s chip exports are booming, but domestic value capture remains low. To stay competitive under trade pressure, Vietnamese conglomerates must invest in high-value segments and ecosystem building.

Problem

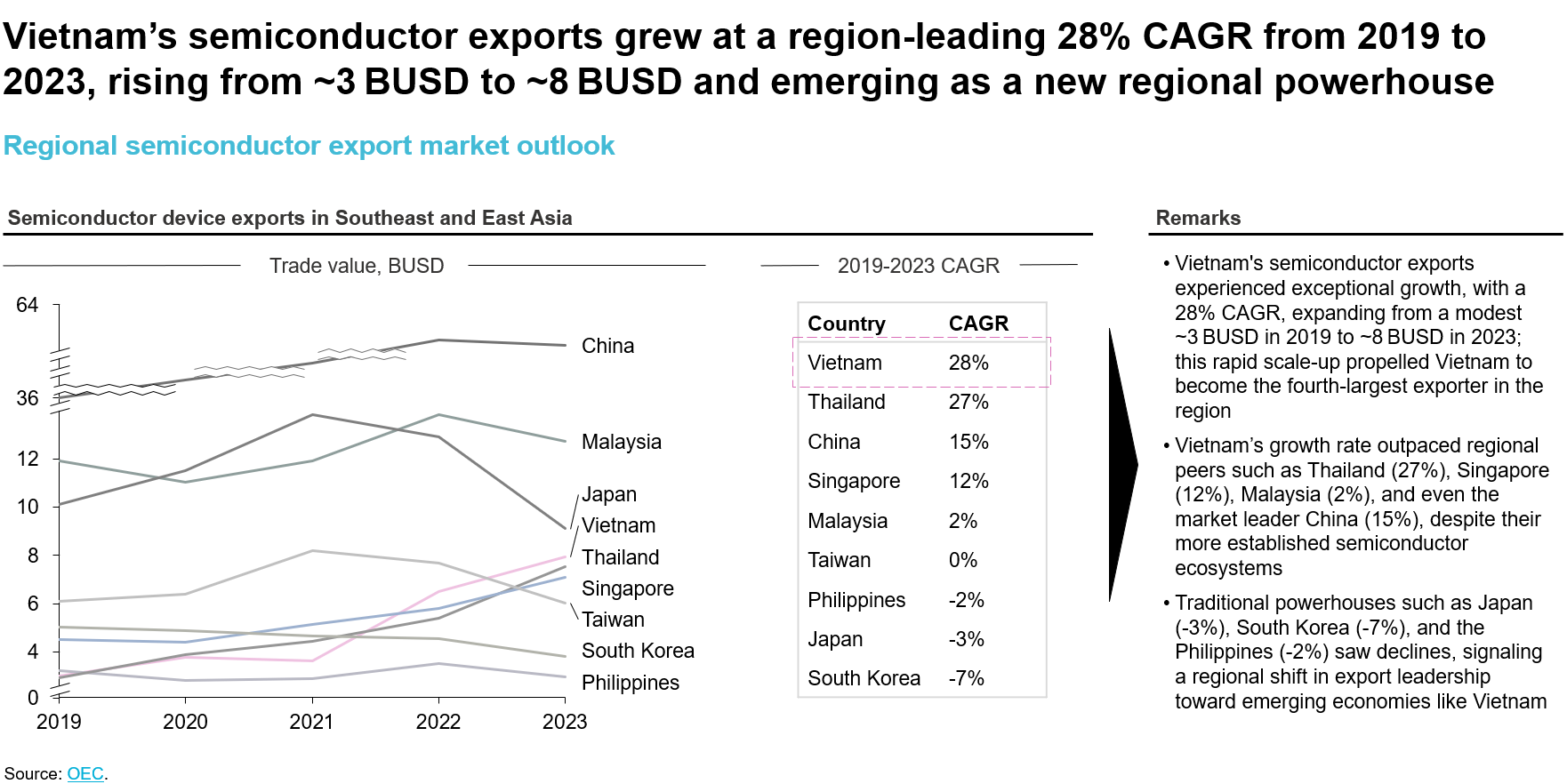

Vietnam’s semiconductor exports surged from ~3BUSD in 2019 to 8.1BUSD in 2023, yet domestic companies contribute to only a narrow portion of the value chain. This leaves the country vulnerable to new trade tariffs and limits its strategic role in the global semiconductor ecosystem.

Why it happens?

Vietnam’s export growth has been led by foreign ATP investments, while design, fabrication, and materials production remain mainly external. Domestic firms lack access to high-value segments and must rely on imported inputs, creating exposure to compliance risks and diminishing profit margins.

Solution

Domestic conglomerates should focus on: (1) capital-efficient, high-impact manufacturing investments, (2) localization of input supply, and (3) building certified talent pipelines with embedded compliance systems. These moves will reduce trade risk and strengthen domestic value creation.

Download this post (PDF)

Export volumes are rising, but value creation is happening elsewhere

Vietnam’s semiconductor exports jumped from 3.2BUSD in 2019 to 8.1BUSD in 2023, establishing the country as Southeast Asia’s fastest-growing chip exporter[1]. Companies like Intel, Samsung, and Amkor have expanded operations, with Amkor committing 1.6BUSD to build its largest ATP (assembly, testing, packaging) facility globally in Bac Ninh[2]. Vietnam is also taking its first steps into domestic ownership with a locally built chip plant scheduled to launch in 2026[3].

Yet, despite strong export momentum, most of the value is not captured locally[4]. Today, Vietnam contributes primarily to low-margin assembly activities, while IP development, chip design, fabrication, and upstream materials remain abroad. As a result, both profit margins and strategic control remain limited. This has prompted the government to set a clear target: significantly raise Vietnam’s value-added rate in semiconductor exports, supported by local ecosystem development and technology adoption.

Policy ambitions are strong, but execution power must come from the private sector

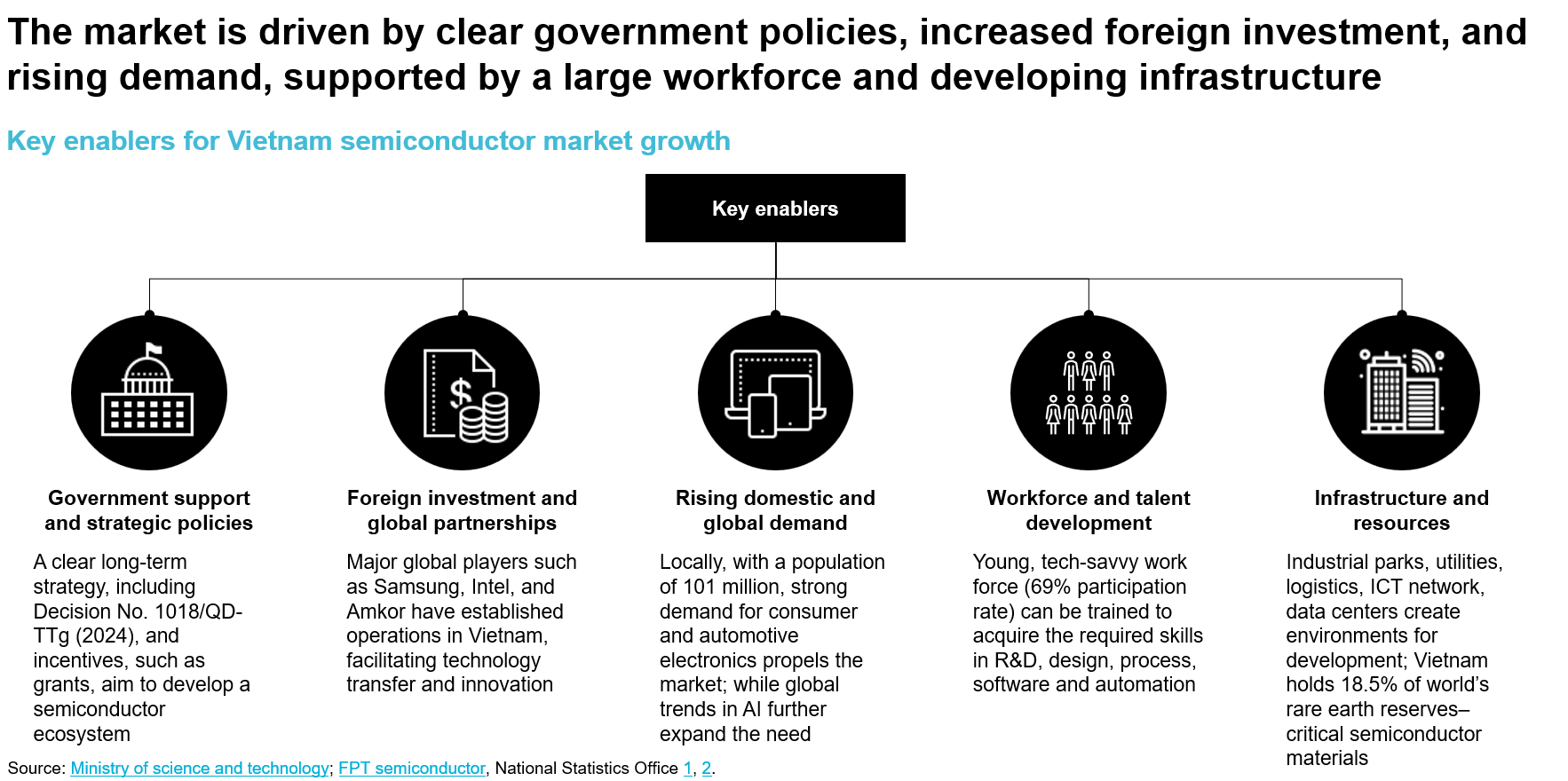

Vietnam’s semiconductor roadmap – Decision 1018/QĐ-TTg – sets bold national objectives: over 100 local chip design firms, 10 advanced packaging plants, and 50,000 trained engineers by 2030. Initiatives led by the Ministry of Industry and Trade (MOIT), National Innovation Center (NIC), and local universities are being coordinated to provide tax incentives, public funding, and infrastructure planning.

Importantly, in August 2025, Vietnamese authorities announced a new ambition: by 2027, essential semiconductor chips should be designed, manufactured, and tested entirely within the country[5]. This timeline reflects rising urgency amid trade policy shifts and technological competition.

However, policies alone cannot deliver transformation. Deep industrial change requires leadership from established domestic firms – those capable of absorbing long investment cycles, building technical teams, and investing in capability development. Vietnam’s private sector must now step up as co-drivers of its semiconductor ambitions.

Tariffs are rewriting the rules - and local value is the key to resilience

In July 2025, the U.S. introduced a 20% tariff on Vietnamese exports, alongside a 40% penalty on transshipped goods, aimed at reducing third-country circumvention of trade restrictions. In August, a more targeted policy followed: a 100% tariff on imported semiconductor chips, unless they are manufactured in the United States[6], [7].

These measures increase compliance risk for chip exports that rely heavily on foreign inputs or ambiguous value-added structures. Without increased localization of high-value processes, many current exports may face higher duties or reclassification – undermining Vietnam’s competitive advantage.

Vietnam need not start from scratch. The strategic blueprints of Asia’s semiconductor powerhouses offer references for inspiration:

- South Korea succeeded by enabling conglomerates like Samsung to vertically integrate design, wafer production, and packaging – retaining value within national firms

- Japan maintained a niche dominance in photomasks, materials, and ultra-precision manufacturing tools

- Taiwan built a dense ecosystem anchored by TSMC, with strong linkages between government R&D, universities, and specialized SMEs

These models differ, but they all highlight a common truth: while state strategy matters, industrial outcomes are driven by private-sector execution. Vietnamese firms must not wait for specific top-down solutions – they must claim leadership roles across the value chain.

Strategic roadmap for domestic firms: Capturing higher value by 2027

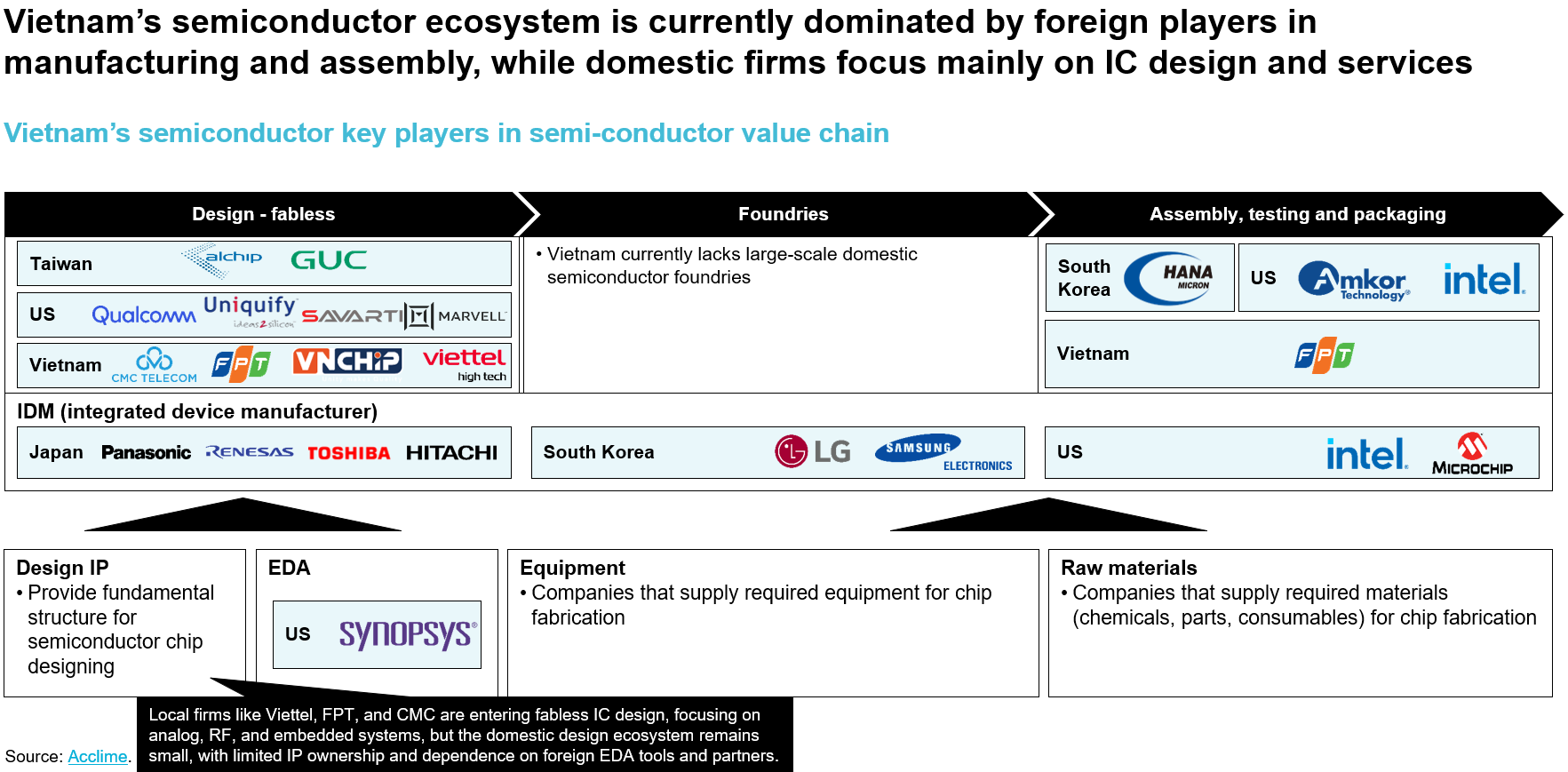

Vietnam has made credible initial steps. FPT Semiconductor launched design activities and is building a chip testing factory in Hanoi[8]. Viettel has committed to establishing a domestic chip foundry. Foreign ATP investments from Hana Micron and Amkor are expanding, while Vietnam's entry into global semiconductor alliances shows geopolitical alignment[9], [10].

But to reach the 2027 goal of end-to-end domestic chip production, three strategic actions are required:

1. Build scalable and integrated design, manufacturing, and testing capability

Domestic firms must accelerate capital deployment in segments where Vietnam can realistically build competitive advantage. Pilot-scale foundries could be operational by 2026–2027 if backed by large conglomerates. Similarly, ATP capacity should shift toward domestic ownership with certified infrastructure, while fabless design capacity must move from academic labs to commercially validated IP.

2. Localize input materials and compliance systems

Many essential inputs – substrates, bonding wires, testing consumables – are currently imported. Domestic firms should pursue joint ventures or sponsor upstream manufacturing of selected inputs to raise in-country transformation. Simultaneously, traceability and compliance systems must be installed to validate Change in Tariff Classification (CTC) during customs review.

3. Strengthen human capital and embedded R&D ecosystems

Vietnam faces a bottleneck in skilled semiconductor engineers. Domestic firms should work with universities and NIC to co-develop specialized programs in EDA (electronic design automation), packaging, chip testing, and verification. These should be paired with R&D labs that support chip prototyping and materials science, paving the way for long-term IP ownership.

If Vietnamese conglomerates commit to these pathways now, the country can meet its 2027 ambition and position itself as a resilient and credible node in the global semiconductor value chain.

Conclusion: Vietnam’s semiconductor future depends on domestic execution

Vietnam has proven it can attract world-class semiconductor investments. But in a landscape shaped by shifting trade rules and rising strategic competition, the next phase must be different. To retain export competitiveness and unlock higher value, Vietnamese firms must take deeper ownership of manufacturing, materials, and compliance.

Success will depend not on replicating past models, but on bold leadership – strategic investment, ecosystem development, and a commitment to building capabilities at home. If these moves are made now, Vietnam can move beyond being a fast-growing exporter to become an essential contributor to the regional semiconductor value chain.

References:

[1] OEC Semiconductor devices (2025) retrieved at https://oec.world/en/profile/hs/semiconductor-devices on 30 October 2025

[2] VnEconomy (2023) retrieved at https://vneconomy.vn/nha-may-ban-dan-lon-nhat-the-gioi-cua-amkor-tai-bac-ninh-chinh-thuc-di-vao-hoat-dong.htm on 30 October 2025

[3] Vietnamnet (2025) retrieved at https://vietnamnet.vn/en/vietnam-to-build-its-first-locally-owned-semiconductor-plant-launching-in-2026-2380735.html on 30 October 2025

[4] WTO (2024) retrieved at https://www.wto.org/english/res_e/publications_e/gvc_dev_rep23_e.htm on 30 October 2025

[5] VnEconomy (2025) retrieved at https://en.vneconomy.vn/essential-semiconductor-chips-expected-to-be-designed-manufactured-and-tested-by-vietnam-no-later-than-2027.htm on 30 October 2025

[6] Reuters (2025) retrieved at https://www.reuters.com/world/china/trump-says-us-levy-100-tariff-imported-chips-some-firms-exempt-2025-08-07 on 30 October 2025

[7] Vietnam Briefing (2025) retrieved at https://www.vietnam-briefing.com/news/new-tariffs-on-vietnamese-exports-analyzing-the-new-tariff-framework.html on 30 October 2025

[8] Reuters (2025) retrieved at https://www.reuters.com/technology/vietnam-expands-chip-packaging-footprint-investors-reduce-china-links-2024-11-12/ on 30 October 2025

[9] Astutegroup (2025) retrieved at https://www.astutegroup.com/news/industrial/vietnam-steps-up-as-global-semiconductor-players-exit-china/ on 30 October 2025

[10] Semi (2025) retrieved at https://www.semi.org/sea/blogs/Vietnams-Semiconductor-Pivot on 30 October 2025

Tags

Vietnam, Vietnamese market, Semiconductor, Semiconductor ecosystem