Using success gates in portfolio strategy development for more informed decision making

9 September 2021 — Developing a portfolio strategy is complex due to numerous opportunities, limited resources, business constraints, and market uncertainties. Defining key constraints for individual portfolio businesses and using success gates to track their impact helps in selecting viable strategic options for all future scenarios.

Problem

In a corporation with a portfolio of businesses, decision making is often complex due to multiple strategic options. Capital and human resources are typically limited when compared to available strategic options and actions. Future scenarios and their impact on strategic options are also uncertain. Management tries to decide the right portfolio development actions to maximize the value of the corporation, but a synthesized view on the best solution may be missing.

Why it happens?

There is not enough information or evidence available to make conclusive strategic decisions between portfolio business units. External factors are creating constraints for the outcome of the decisions, making quantitative assessment difficult. Market and technology development affect industry dynamics and drive the need for critical capability building. The trends are also different among the units in a business portfolio. In addition, portfolio options are often cross coupled.

Solution

A structured decision process with success gates helps to select best viable strategic options in a particular future environment. The decision process starts by defining and listing all logical strategic options and critical constraints for each portfolio business. Constraints are prioritized and success gates are defined to measure them. Occasionally outcomes become clear later in time, which allows further data gathering in the implementation stage, before final decisions.

Download this post (PDF)

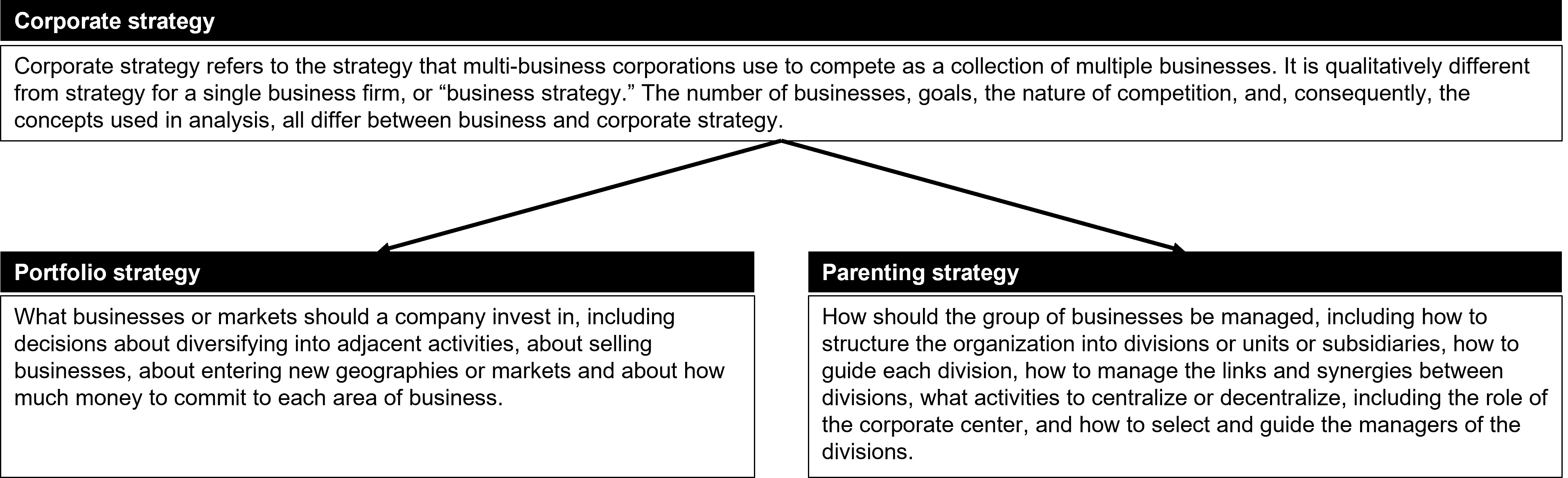

Corporate strategy is about decisions on how to deploy limited resources across the business portfolio and how to define the role of the corporate center

When forming corporate strategy, executives must analyse and decide on two separate components: portfolio strategy and parenting strategy (see also figure 1). In a nutshell, portfolio strategy seeks to maximize owner value by finding out the right investments and divestments in a portfolio of business units. Thus, in a portfolio strategy, corporate-level management sets guidelines for business units to be prioritized, grown, and invested in as well as those that are divested or used as sources of cash. Parenting strategy, in turn, decides the role and responsibilities of the corporate center in serving, structuring, and managing business units. The main evaluation criterion of parenting strategy relates to the comparison of the value of portfolio under the corporate to the sum of the valuations of each business unit as separate entities. The value of a corporation should be bigger than the sum of its parts or in other words, parenting strategy must be value-adding. Should this not be the case individual businesses would be better off as standalone companies.

Portfolio strategy often introduces cross coupled issues, making it hard to synthesize a clear path to an optimal solution

In portfolio strategy executives must decide on the right portfolio development actions required to maximize the value of the corporation. Activities for meeting strategic objectives are often organized by first identifying many alternatives without considering limitations. This is followed by selecting those that are expected to best contribute to reaching the objectives, considering available resources, time and capabilities. The task of assessing portfolio development actions becomes quickly complex. Typically, there are multiple distinct businesses to which limited financial and human resources must be optimally allocated at same time as external changes affect future market development.

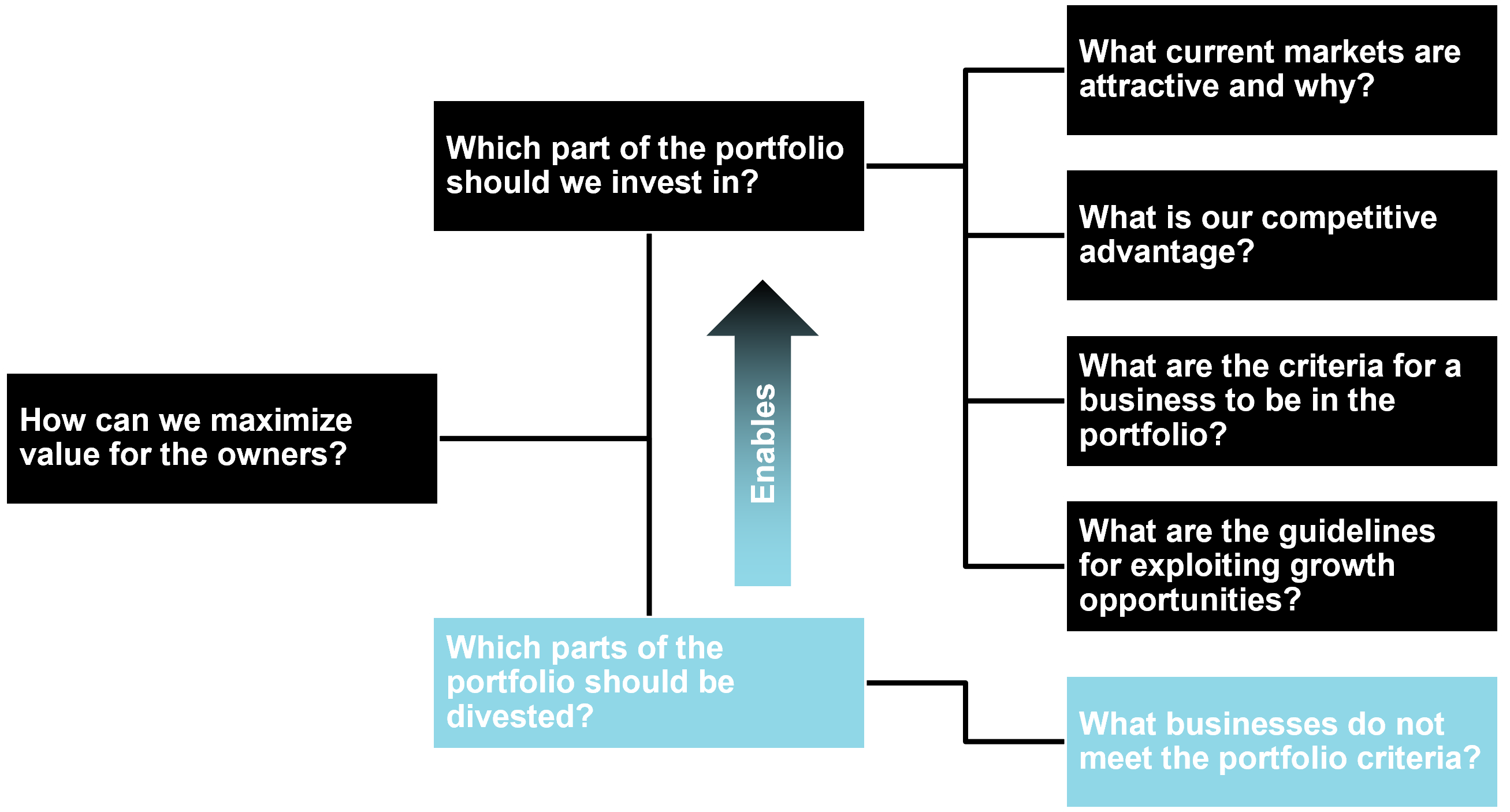

Thus, there are numerous possible strategic options on the table. To narrow them down, corporate executives may leverage strategic ambitions set in corporate strategy, as they give guidance on the criteria for businesses to be in the portfolio. Thus the first step is to prioritize the targeted value drivers of higher growth, reduced costs or optimized capital employed. In addition, typically some portfolio synergies are expected from the businesses. Once these criteria (that is, constraints) are clearly defined (and prioritized), the next phases of portfolio strategy formation generally involve portfolio business unit evaluation, investment process, and portfolio governance.

In portfolio business unit evaluation, the objective is to understand how the units can perform against the criteria outlined in strategic ambitions, how much development potential there is and how the corporate can exploit the opportunities. It should be also noted that portfolio strategy does not create individual business unit strategies or business plans; instead, they act as the basis for business unit evaluation. The evaluation can be done via analysing the market outlook, competitive position, synergies to other units, financial performance as well as required investment needs (including M&A) of the unit to reach its strategic targets (see also figure 2). Linked to investment needs, capability assessment uncovers the current abilities to exploit growth opportunities and whether it is cheaper to develop missing capabilities internally or acquiring them externally. After analysing all these aspects, one can conduct valuation for the units and see how they contribute to the overall corporate value, and what the stand-alone value would be for them as independent units.

Based on portfolio business unit evaluation, executives have a baseline for prioritization of portfolio investments. In addition, the businesses that do not meet the strategic criteria, do not have enough upside potential (even after synergies) or have a higher price available in capital markets than their net present value of future cash flows should be divested. What then follows is the actual deployment process of implementing the investments and divestments that maximize corporate value, together with follow-up mechanisms and overall process governance.

External factors often create uncertainty for strategic options making it hard to assess the realistic likelihood of investment success

Developing and implementing a portfolio strategy sounds simple and straightforward on paper, but in reality this is often not the case. There are typically several industry-specific external factors affecting the operative business environment. Hence, there may be situations where the external factors create critical constraints for portfolio strategy, and these constraints appear distributed over time (that is, along the implementation timeline). This makes portfolio strategy more complex than a straightforward comparison of business units based only on financial estimates.

Examples of such external factors include the pace of technological development, emerging substituting products in the market, uncertainty over future regulatory changes or changes in consumer behaviour. Here we exclude generic completely unforeseeable events and focus on well defined events that have a binary outcome (or potentially multi-dimensional but clearly defined set of outcomes). For such events, there is a set of outcomes for each event, where impact on the business may be substantial. For example, missing the next wave of technological development may turn some business’ existing assets worthless, or decrease their value significantly. The changes in external environment may force some businesses to rapidly refocus to new markets or to acquire new critical capabilities. Yet, while the outcome may be uncertain, it will be (or needs to be) determined by a certain point in time. Further, this point in time fits inside the strategy implementation timeline.

Thus, having identified this type of events, there is a conditionality in portfolio investment decision-making, that then determine whether a strategic option will pan out. The executive problem is that there is not enough information yet available to make final portfolio decisions. Because investment and divestment decisions are conclusive, it is not desirable to make financial decisions hastily (nor walk away from opportunities too easily). Hence, improving the strategy methodology in a way that allows time-delays and impact of future events (or achieved future progress) influence major decisions would be beneficial.

Combining portfolio analysis with success gates methodology helps to see time-dependent constraints, and presents a clear path to the solution

A simple portfolio investment prioritization is based on value creation potential comparison of business units. But selecting the right portfolio development option is more complicated when value creation potential is affected by various (time-dependent) constraints that have an impact on the success of the selected option and actions. Using the conditionality between different constraints to create a logical decision process can help managers make informed decisions. In a recent engagement, we applied a methodology to create a decision process by defining the hierarchy of various constraints and setting up measurable success gates based on these. This helped identify viable strategic options for a corporation with two distinct business units operating in different industries.

Success gates are often used in strategy implementation to track progress and decisively adjust the implementation roadmap end-to-end (when success gates are not met). They are essentially key milestones that can be tracked to ensure that a project is heading towards the strategic end-goal. If a gate is not cleared, then (all) future actions and timelines need to be re-evaluated and re-planned. Success gates are usually designed by first defining the desired end state and then planning backwards to define sequential prerequisites to reach the targeted outcome. In the specific case described here, success gates were designed based on the constraints affecting the viability of strategic options. Then a sequential structure was created by defining a hierarchy for the constraints.

An easy way to define the hierarchy between the constraints is by considering their chronological order. Information on the presence or impact of some constraints can be used for decision making earlier than others. The actions to eliminate these constraints should be made first and these constrains are higher in the hierarchy. Alternatively, if there is no clear chronological order or the timing of the actions required to eliminate the constraints is not clear, the constraints can be evaluated based on the investments required to eliminate or resolve the constraint. In that case, the costliest constraints should be higher in the hierarchy; the decision on those actions should be made first. If the investment amount differential is negligible, one can also consider the opportunity costs of waiting.

The hierarchy of the constraints is used to set success gates in sequence to create a decision process. Each success gate should determine whether the given constraint has been eliminated. Starting from the current state and connecting all the success gates, a logical decision process is created. This forms a tree-like structure, where the combinations of constraints create all the scenarios affected by the constraints. Understanding the constraints in all scenarios helps to select the most viable strategic options for each scenario. Using success gates to form a logical decision process is illustrated in figure 3.

Expanding simple portfolio strategy with success gates builds a more robust view on viable strategic options and the path to solution

Using success gates to create a decision process in portfolio investment decision-making helps executives make informed decisions when valid evidence is available. The success gate structure can be used as a tool for prioritizing decisions and understanding the connections between separate decisions. This also helps in assessing the likelihood of certain future scenarios as it clearly shows what constraints are related to each scenario and what actions must be done to eliminate those constraints. To use this methodology for decision-making, management must commit to the process and how success gates are used. Success gates must be clearly defined so that there is no room for interpretation. It should be noted that a success gate structure inherently contains major risks and contingency plans, thus having a “built-in” risk mitigation plan the implementation phase.

This methodology is not without limitations. It works best in situations where two (or a limited number of) portfolio units are compared, and the decision how to allocate investments between these. The success gates are binary (or at least measurable with a clear threshold point on a continuum) so they are typically straightforward to handle. However, when the number of constraints grows, and investment allocation decisions involve more than a few units, the decision process mapping quickly becomes too difficult to follow. Despite this limitation, the methodology is still applicable in many large corporations.

Combining two classical strategy tools, portfolio strategy analysis and success gates, provides a new approach for structured decision making in strategy work. In a complex, constantly changing environment it is impossible to set up a structural framework for decision making, that provides a path to solution and has built-in contingency plans.

References

Campbell, A., Goold, M., Alexander, M., & Whitehead, J. (2014). Strategy for the corporate level: Where to invest, what to cut back and how to grow organisations with multiple divisions. John Wiley & Sons.

Liesiö, J., Salo, A., Keisler, J. M., & Morton, A. (2020). Portfolio decision analysis: Recent developments and future prospects. European Journal of Operational Research.

Gupta N. (2016) Using decision gates to give project milestones real teeth, McKinsey Quarterly 2016

Porter, M. E. (1989). From competitive advantage to corporate strategy. In Readings in strategic management (pp. 234-255). Palgrave, London.

Puranam, P., & Vanneste, B. (2016). Corporate strategy: Tools for analysis and decision-making. Cambridge University Press.

Rosenzweig, P. (2014) The benefits – and limits – of decision models, McKinsey Quarterly February 2014

Tags

Success gates, Decision-making, Portfolio management, Portfolio strategy, Corporate strategy