Identifying investment targets through future-looking industry analysis

11 October 2022 — Traditionally, private equity (PE) sourcing relies on networks and industry screening, causing leads investors to compete for the same targets. Conducting future industry analysis can give PE investors an edge, identifying emerging opportunities early and building a competitive advantage.

Problem

There is a limited number of good targets for private equity firms, hence competition for the best investment cases is driving valuations up and returns down. The challenge is how an investor can identify targets before others.

Why it happens?

Most private equity firms deploy similar deal sourcing strategies leveraging industry expert networks and focusing on “hot” industries, copying what others are doing. This easily leads to increased competition for targets in one area.

Solution

Taking a systematic future-looking and holistic approach to determine whether the right preconditions exist for successful private equity value creation strategies can help an investor to gain an edge in identifying potential industries and targets earlier.

Download this post (PDF)

In this article we start by asking the question “is it possible to gain an advantage in terms of early identification of attractive investment targets in mid-cap private equity”. We chose mid-cap because in this category the companies that are attractive to private equity typically already have a long history. At the same time, mid-cap industries are often not extensively covered in media and thus it should be possible to gain an information advantage through solid research. Thus it seems feasible that one could, by applying the right methodology, be able to identify attractive industries and investment targets within them already long before the industry actually becomes “hot”.

We focused our research on Finnish mid-cap private equity investors and their past investment decisions. Our data shows that, in general, investors tend to flock to the same industries in a fairly synchronized way. Clearly, industries and companies in them go through a development cycle so that at some point the circumstances are correct for private equity engagement. The industries that end up being targeted have evolved so that within them specific value creation strategies become available, and investments have a high likelihood of a positive return.

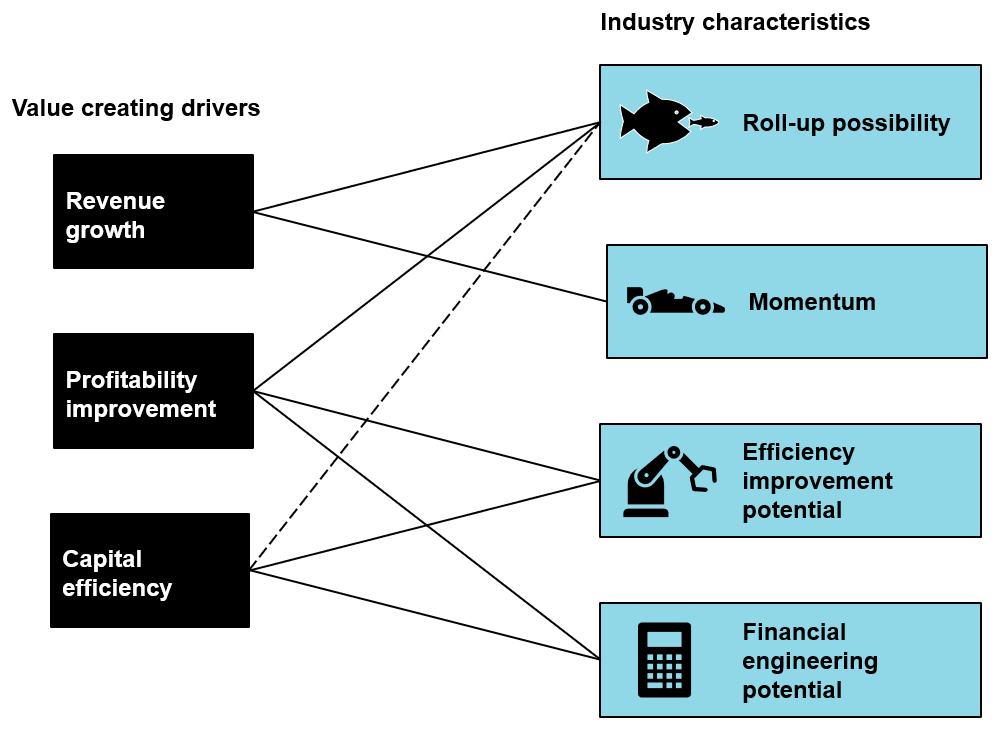

To simplify PE value creation, there are three main drivers for value creation: revenue growth, profitability improvement and capital efficiency improvement. Investors use various strategies to capture at least one of the drivers and increase the value of their investment.

By studying recent “hot industries” in private equity, we can identify key industry characteristics which signalize a more favored ground for the drivers to be successfully captured. The characteristics include roll-up possibility, momentum, efficiency improvement and financial engineering potential.

Roll-up possibility refers to the opportunity to use the so-called “buy-and-build" strategy for value creation. M&A activity can be used to grow portfolio company’s topline and consequently capture more market share. For an industry to be suitable for a roll-up, there needs to be enough potential add-on acquisition targets available, and the industry must be still rather fragmented when looking at the largest companies’ market shares.

Momentum refers to a clear trigger for demand growth, such as changes in regulation or technology adaptation. Changes may for example allow private companies to enter previously regulated markets and grow aggressively to capture market share.

Industries with efficiency improvement potential are usually seen as stagnant and lacking innovations. Value can be created by boosting investments and accelerating the adaptation of new technologies to increase productivity. Investors can also create value by achieving profitability improvements through economies of scale. Often economies of scale are achieved also with the buy-and-build strategy.

Financial engineering potential offers an opportunity to create value by lowering the cost of capital. Increasing company leverage (to a certain point) lowers the total cost of capital and enables creating more value for the owners. New debt can be used to accelerate investments to improve profitability. Industries with financial engineering potential are often distinguished by low levels of leverage and positive operative cash flow.

Even one of these key characteristics can make an industry attractive for PE investors but often there are two or more present. By looking for these characteristics in an industry, PE companies could identify future hot industries earlier or identify emerging value creation opportunities before their competitors. We developed a simple methodology for future-looking screening of potential target industries using the industry characteristics. The methodology consists of three steps:

- Select a value creation strategy and define metrics for the industry characteristics that support the selected strategy

- Use the defined metrics to identify potential industries and narrow down industries using other characteristics supporting the value creation strategy

- Select suitable target companies by conducting more research on the industry

Let us now illustrate this methodology by a practical example.

Step 1: Select a value creation strategy and define metrics for the industry characteristics that support the selected strategy

We selected the number of potential acquisition targets as the first screening criteria as a good indicator for the roll-up potential of an industry. Roll-up potential has been important for PE value creation in recent years as the so-called “buy-and-build" strategy has been a popular strategy among investors. There are multiple examples of PE companies executing the strategy successfully in recent years, for example in accounting services and real-estate management, and more recently in various professional services categories.

Buy-and-build and aggressive inorganic growth may not be the only viable strategy in the industries we find in the screening, but we use it as our “hypothesis” in order to find interesting industries with value creation potential.

For roll-up potential, we want to find industries that have multiple companies with suitable revenue levels. The target companies cannot be too big for an acquisition or too small for a merger to add value. The target companies should also operate in markets that are not dominated by only a few large players. For this we want to find industries where the largest companies have less than 40% of the market share, since want to have room to grow in the market and avoid fierce competition for the target companies.

Step 2: Use the defined metrics to identify potential industries and narrow down industries using other characteristics supporting the value creation strategy

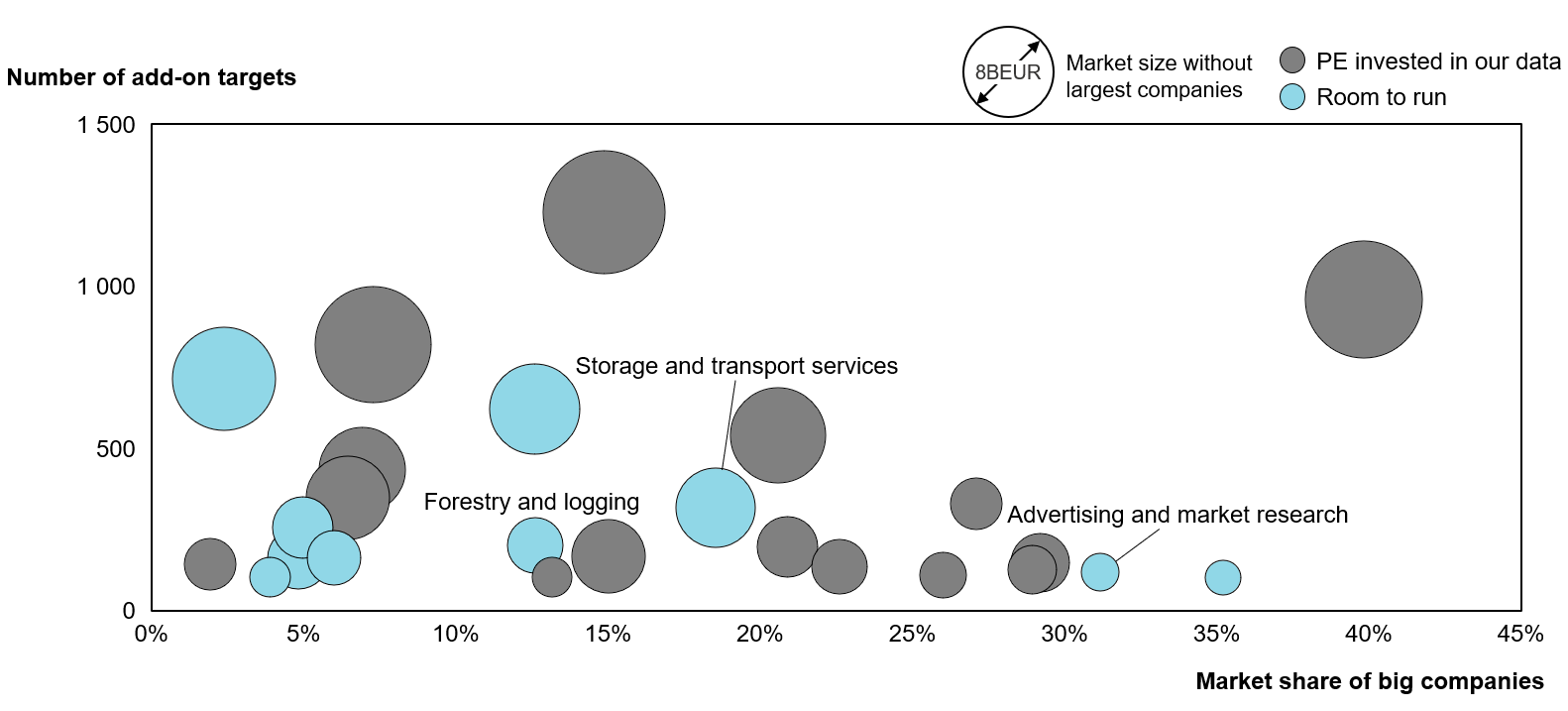

At the time of this analysis, in Finland there were 25 attractive industries for a buy-and-build strategy by using several add-on-targets and market share of the biggest companies as screening criteria.

After identifying the industries with roll-up potential, we wanted to understand other characteristics and value creation drivers in the industry. For example, is there anything creating momentum to support value creation? Perhaps megatrends or changes in legislation that can support market growth. We were also interested in identifying potential efficiency improvement opportunities such as possible investments in new technology. Research on the key value creation drivers was used to further narrow down the industries. The results of the initial screening are illustrated in figure 2.

With our approach we could identify forestry and logging services, storage and transport services and advertisement and market research as interesting industries where there could be potential to create value. All these industries had momentum to support growth; new technology for the last two and changes in regulation for forestry and logging services. There were also possibilities to improve operational efficiency in all of these industries.

Phase 3: Finding target companies with deeper analysis of identified industries and picking category winners with best fit to the strategy

The final step in our methodology is what is traditionally considered as investment target screening. Different players are assessed within the interesting industries in order to filter out the most potential candidates for the acquisition. The aim is to pick the potential category winners that have the best fit to the value creation strategy and the value creation drivers. Here traditional financial metrics such as revenue, growth and profitability were used. For the buy-and-build strategy, we wanted to find a platform company and grow it to become an industry leader by adding smaller complementary competitors to the platform and developing the product or service portfolio. The right circumstances for this needed to be present in the industry, or alternatively, we wanted to see that this type of industry dynamics would be a likely outcome of the present evolution.

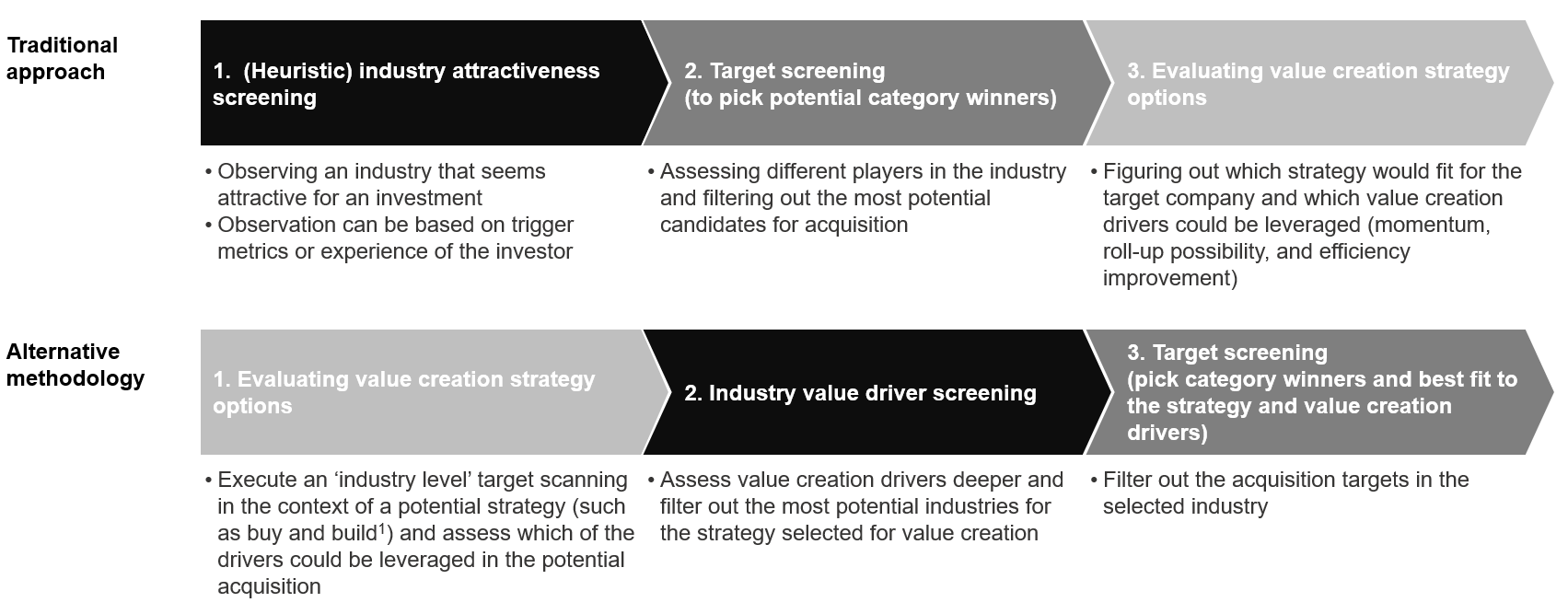

The future looking methodology can be used as a complement to traditional approaches and can provide an edge if applied systematically

To summarize, our methodology takes a broader perspective on PE investment screening. Instead of focusing the screening on attractive industries, we start by evaluating value creation strategy options and looking for industries that offer potential for a particular strategy. Figure 3 illustrates our methodology and its difference from a more traditional approach to PE investment screening.

This value creation strategy driven screening can help investors discover future hot industries and potentially open discussions with investment targets before competitors. Additionally, when opening the discussions, there is a thought-through value creation strategy already in place to be proposed. Finally, as this methodology can help PE firm to find the target without too much competition, it will help boost its investment returns over the investment holding period.

Tags

Private equity, Merger and acquisition, investment, Target screening, Value creation, Methodology, Industry analysis